This was our Feature story in the Oddball Stocks Newsletter, Issue 31, in August 2020.

We pointed out that small bank stocks had crashed with coronavirus in the spring and represented an interesting recovery trade.

Looking for value in the overlooked margins of the market.

This was our Feature story in the Oddball Stocks Newsletter, Issue 31, in August 2020.

We pointed out that small bank stocks had crashed with coronavirus in the spring and represented an interesting recovery trade.

The quarterly report from Hanover Foods for the period that ended August 29, 2021 shows that sales, gross profit, operating expense, and net income all dropped versus the prior year's quarter.

The company spent $6.4 million on “acquisitions of property, plant and equipment” last quarter. Over the past five fiscal years (not including the recent $6.4 million), the company has spent an immense amount on capital expenditures, a total of almost $80 million dollars.

It is hard to know what this $80 million of capital expenditure has accomplished for shareholders without any disclosure of what it was spent on. Certainly, it is difficult to see in the financial statements that this has been a worthwhile expenditure of capital.

All that we can see is that assets (both current assets and property and equipment) are growing, but seem to be generating less revenue. Asset turnover is slowing. Revenue, gross profit, and operating profit were all lower in fiscal 2021 than they were in fiscal 2017. And since cash from operations has not been sufficient to pay for the capital expenditures, debt has been rising, from total liabilities of $63 million in May 2016 to $106 million in August 2021.

Hanover Fiscal Q1 2022 Earnings by Nate Tobik on Scribd

Our past posts on Hanover Foods:

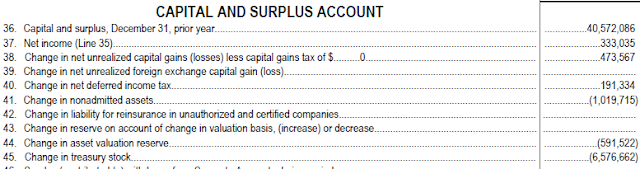

There is something interesting on page 5 of the quarterly statement for Life Insurance Company of Alabama (LICOA) for Q3 2021.

We knew that on June 14th, a block of 205,221 LINSA (LICOA non-voting) shares had traded for $24 per share, and that the same block traded again on July 22nd for $32 per share. But we did not know who had bought for $24 (a $4.9 million purchase) or $32 ($6.6 million).

However, we now see that LICOA's regulatory financial statements for the third quarter of 2021 disclose a $6,576,662 purchase of treasury stock. That would be $32.05 per share if it was that same block from July. That purchase price was well below book value (approximately 75% of statutory book), and it was for a huge percentage (~20%) of the company, so the result is very accretive to book value.

LICOA borrowed $6,600,000 from the Federal Home Loan Bank of Atlanta in connection with the share repurchase. Perhaps management has finally figured out that it makes sense to replace outside shareholder capital with cheap debt, especially if shares can be had at a discount to book value.

The minority shareholders who sued the company in the US District Court for the Northern District of

Alabama in 2019 are awaiting a ruling from the court on the company's motion to dismiss their case. Be sure to check out the Concerned Shareholders of Life Insurance Company of Alabama website as well.

LICOA Quarterly Statement Q3 2021 by Nate Tobik on Scribd

Previously, regarding Life Insurance Company of Alabama:

Friendly Hills Bank is a small bank in Whittier, California (a city in Los Angeles County) that was founded as a community bank in 2006. The shares are OTC-listed (ticker FHLB) and trade for around $10, which is about the same as the IPO price a decade and a half ago. We did several posts about rising activist pressure at FHLB earlier this summer:

Since we last wrote about it, the company has announced that incumbent CEO Jeffrey K. Ball, Chief Executive Officer is moving on to greener pastures, "in connection with his desire to pursue other business opportunities."

We also saw that Frank Kavanaugh, a long-term shareholder of Friendly Hills Bank, released a public letter to shareholders of FHLB yesterday:

November 22, 2021

Dear Fellow Friendly Hills Shareholders,

We are a group of shareholders that represent more than 25% of the outstanding shares of Friendly Hills Bank (“Friendly Hills” or “the Company”). We have long been concerned and dismayed by the inability of management and the Company’s board of directors (the “Board”) to create value for shareholders, and we believe that it is time for that to change.

Soon, you will receive proxy materials from us in which we outline our vision for a better future for the bank and its employees and customers. In our view, any change must start by refreshing the Board with the addition of new, independent members who understand the bank, its history and its mission, and who are committed to make Friendly Hills responsive to its stakeholders rather than a piggybank for its current Chairman, Vice Chairman, and CEO.

We urge you to consider the following recent failures of the Company’s management and Board, which we believe have destroyed tremendous value for shareholders:

We believe Friendly Hills urgently needs new independent directors who will advocate for shareholder rights and interests. With the departure of the CEO, the board will select the direction and leadership for the future. The CEO, Chairman, and Vice Chairman have not generated value for shareholders in over 15 years, and they have not been held accountable. The Bank needs leadership focused on creating value for Friendly Hills’ owners – its shareholders – we need a Board with a demonstrated track record of successfully building community banks. Join us in creating a strong future for Friendly Hills Bank, its employees, and shareholders. Help us hold the Board leadership accountable at this critical juncture.

We urge Friendly Hills’ shareholders NOT to respond to solicitations made by the Company, its current management, or the Board until you have received our proxy material.

We would value your feedback. Please contact us at 949 212-2222.

Big news announced this evening from Keweenaw Land Association (KEWL):

Keweenaw Land Association, Limited (OTC US: KEWL) today announced it has entered into a definitive agreement to sell its timber assets to an entity managed by a non-affiliated large institutional timberland investment manager in an all cash transaction. The transaction is expected to close by the end of 2021, subject to shareholder approval, completion of buyer’s inspection period, and other customary closing conditions. Keweenaw will retain ownership of 428,789 acres of subsurface mineral rights and will continue to trade as a public company while the board continues to explore the most efficient structure for its remaining assets.Nate first wrote about Keweenaw ten years ago: "A small cap pure timber play". The price before this announcement was exactly the same as when he wrote it up, and it has not paid a dividend over the past decade. We wrote about KEWL in Issue 20 of the Newsletter (June 2018):

The company also announced that its board of directors approved a plan of partial liquidation in connection with the sale (“Plan of Partial Liquidation” or “Plan”). If the Plan of Partial Liquidation is approved, the net proceeds from the sale following the deduction of corporate taxes, other expenses related to the sale, cash retained for the ongoing business, and an indemnity holdback, will be distributed to the company's shareholders. We estimate this special distribution will equal approximately $100 per share, payable in two installments as follows: an initial distribution of approximately $92 per share payable on or before December 31, 2021, and a second distribution of approximately $8 per share payable on or before December 31, 2022. The second distribution is subject to potential reduction for indemnity claims or other contingencies.

It is intended that the special distribution will be treated as a “redemption in partial liquidation of the Company” within the meaning of Section 302(b)(4) of the Internal Revenue Code. Each shareholder is urged to consult and rely on their own tax adviser with respect to the tax consequences of the special distribution.

Notwithstanding the adoption of the Plan, the Company expects to continue operating as a going concern and a publicly traded company focused on maximizing the value of Keweenaw’s remaining assets, including its mineral rights. The Company will take steps immediately upon closing to substantially reduce its overhead costs; most notably by decreasing headcount, board size and professional service fees. Possible savings contemplated at this time include moving from a PCAOB audit standard to an AICPA standard and potentially moving from the OTC Pink Current Tier to the OTC Pink Limited Tier. Tim Lynott will become Keweenaw’s President on January 1, 2022, replacing Mark Sherman who is retiring.

The Company has prepared a proxy statement, which it anticipates mailing to shareholders beginning on or about November 24, 2021.

Keweenaw is a forest products and land management company located in Ironwood, Michigan. Keweenaw has land holdings of approximately 185,000 surface acres and owns over 400,000 acres of mineral rights, located predominantly in the western Upper Peninsula of Michigan and in nearby northern Wisconsin. The company is really just a timber company right now, but they are hoping that Highland Copper Company will be successful with its Copperwood project on some of the company's land (the last time they had mining income was in 1994).

The history of the company dates back to something called the Portage Lake and Lake Superior Ship Canal, built through the Keweenaw Peninsula to reduce the distance that ships traveling Lake Superior would need to travel. The Federal Government granted 400,000 acres of land for the construction of the canal. Some of the land grant ended up being reorganized in 1908 as the Keweenaw Land Association, Ltd as a partnership, and then again in 1999 as a corporation, today’s KEWL.

At the April annual shareholder meeting there was a victory by the activist investors Cornwall Capital Management (who were profiled in The Big Short by Michael Lewis for having put on the mortgage CDS trade). Shareholders elected Cornwall's nominees and professional investors Ian Haft, Steve Winch and Paul Sonkin. Cornwall has owned shares in the Company for over a decade and Jamie Mai, Founder of Cornwall Capital, has served as a director since late 2015. Cornwall’s current ownership is approximately 26% of the outstanding shares. James Mai, who needed to have his nominees elected or he would have been kicked off of he board, is now the Chairman.

The activists put up a website with their proxy statement, a pitch deck with their “Plan to Return Keweenaw to Success,” and their mailings to shareholders of the company. (It would be smart to download these materials now if you are interested in the company, because sites like this do not stay up forever.)

The activists proposed a four point plan. First, re-position the company for cash flow growth by increasing harvest rates, “given sub-optimal historical under-harvesting,” and align the compensation of management and other employees with this objective. Second, reduce costs by reducing board expenses, including eliminating the Chairman's salary and other non-essential board related expenses. Third, improve corporate governance by eliminating the staggered board, the super-majority provisions, and improving disclosure of timber inventory and the quality of communications with shareholders. And fourth, repair the balance sheet by ceasing acquisitions, selling non-core assets, and paying down debt. (The company borrowed $5 million from MetLife in December 2016 at a 3.05% rate for ten years and a further $12.7 million from them in March 2017 at the ten year yield plus 1.5%, for ten year money as well. It probably makes sense to pay off the more expensive money but not the 3.05% loan.)

Dave Waters at OTC Adventures wrote about Keweenaw in October 2015 (well worth reading). At that point James Mai had just come on the board and shares were trading for around $80. With the activist victory (and probably also the increase in timber prices), the shares are now trading for a little over $100. This is no different than where they were trading in 2007. The shares have been dead money for over a decade, and to our knowledge no dividends have been paid since 2009. Owning timber would be very interesting (if it were well managed and in a low-debt company) because you would have an opportunity to play the building cycle. If you have a lean organization with no debt, nobody makes you cut timber when the housing market is in the tank. You can let the trees grow, generating untaxed value, and have them cut when the lumber will command a better price.

The company has 1,301,550 shares outstanding which makes the market capitalization about $135 million. As of the end of the first quarter, the company had net debt of about $15 million which would make the enterprise value about $150 million. For that you get 185,750 surface acres and over 400,000 acres of mineral rights. If you value the mineral rights at zero, then you are paying an enterprise value of about $800 per acre for the timber. Meanwhile, in its most recent major purchase transaction in March 2017, the company bought 14,035 acres in northern Wisconsin from Great Northern Forest for $12.8 million, which was $912 per acre. One bit of interesting sleuthing to do would be to get more details about the aborted effort by Stifel to market the company in 2017 – how do those bids compare to the current market valuation?

Another valuation point was the appraisal commissioned by the company in 2016 by Sewall, which was only for 167,613 acres because it was before the Great Northern Forest transaction. At that time, the estimated value by the appraiser was $151 million which was $901 per acre. The report noted that since 2010 the company had sold 1,600 acres in small sales for $1,525 per acre and bought 8,351 acres in bigger transactions for $954 per acre.

It would be interesting to know why the company made some of those acquisitions when its own stock was trading for less money per acre. Of course, it is obviously possible that the acreage they bought had more mature trees or a more valuable mix of timber. By the way, another interesting way to look at KEWL is that there are 1,301,550 shares which own 185,750 surface acres. So essentially for each share you get about 1/7th of a timber acre (and then your share of net debt).

One funny thing about the current trading price is that lumber prices are up immensely in 2018 and the company is in activists' hands but the share price is not up that much. Timber EBITDA was up 93% in the first quarter compared to the previous year. It will be very interesting to see what the company reports for the second quarter of 2018.

We mentioned it again in the Newsletter in Issue 21

Nate has a theory that activist takeovers should be bought. The hypothesis would be that in those companies, minority shareholders have had dead money for a long time. Sure, the stock might rally when the activists win, but this could be an under-reaction to what better aligned activist investors can do with the underutilized assets.It will be very interesting to watch where the company goes from here. Maybe the Keweenaw copper royalty stub (will they change the name?) buys Pardee Resources in a hostile takeover, fires the expensive board, sells the timber and agricultural investments,and retains the coal royalties and the oil and gas production. Perhaps they could buy Beaver Coal (with its metallurgical coal royalties) for good measure.

We just published Issue 37 of the Oddball Stocks Newsletter. If you are a subscriber, it should be in your inbox right now. If not, you can sign up right here.

Remember that we have made some back Issues of the Newsletter available à la

carte, so you can try those before you sign up for a subscription: Issues 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, and 31. We lowered the price of most of our back Issues to $99 from $139. If you are curious about them, there has never been a better chance to try them.

We also published a Highlights Issue in February 2020. The Highlights Issue is available here for purchase as a single Issue.

If you have been curious about the Newsletter, the Highlights Issue is the perfect

opportunity to try about two Issues worth of content (much of which is

still topical and interesting) at a low cost.